Published Date: 2022-09-28

By Kristy Tsun Tzu

Hsu

September 2022

Semiconductors are

critical for industries in the 21st century. They also play a key role in

defining economic competitiveness and national security, the worldwide

shortages of semiconductor chips in the past years resulting from supply chains

disruption and the COVID pandemic demonstrates the challenge to accessing

semiconductors in global markets. As a result, the United States, Europe, and

Japan have made securing semiconductor supplies as part of their national security

strategy.

The United States

has long felt the side effects of offshoring critical industries to Asia. Since

President Barack Obama’s Reindustrialization Program, both President Donald

Trump and President Joe Biden. continued

to address the supply chains issues while trying to promote manufacturing

industries back to the United States

On February 24,

2021, President Biden signed an Executive Order (E.O. 14017) for a

comprehensive approach to assessing vulnerabilities in, and strengthening the

resilience of, critical supply chains. The Biden administration also took steps

to address supply chain vulnerabilities.1 While the structural weaknesses in

supply chains threatens the U.S. economic and national security, the United

States is nonetheless well-positioned to maintain and strengthen its innovative

leadership and rebuild productive capacity in key sectors and value-chains.

Meanwhile,

President Biden also proposed the Indo Pacific Economic Framework, or IPEF, as

the centerpiece of his economic strategy toward the critical region. The IPEF

consists of four “pillars” of work: (1) fair and resilient trade; (2) supply

chain resilience; (3) infrastructure, clean energy, and decarbonization; and

(4) tax and anti-corruption. The issue of supply chain resilience, both at

domestic and global level, will be reviewed from the Indo Pacific regional

strategic perspective and concrete initiatives and programs are being

discussed.

Taiwan too can

play a key role in the U.S. strategy to reassessing its supply chains. U.S.

initiatives, including IPEEF, the CHIPs and Science Act and other new

initiatives have attracted new investments to reshore industries to the United

States, greater efforts and financial resources are needed to prevent the

current phenomena from becoming short lived. Yet there is a gap between the

U.S. strategy and the business perspectives, with scope for U.S. policy makers

to improve their policy designs to make the semiconductor supply chains more

resilient, stable, and most of all, commercially viable, for U.S. national

interests.

Geographic Specialization and Regionalized

Semiconductor Supply Chains Structure

The semiconductor

industry is technology- and capital- intensive. After more than three decades

of collaboration among countries with their comparative advantages, the global

structure of semiconductor industry today reflects the results of

specialization in various activities in the supply chains. The high degree of

specialization has also led to geographical concentration, making it difficult

for newcomers.

Over 75 percent of

semiconductors in the world are manufactured, or fabricated, in East Asia. The

United States and Europe account for only 13 percent and 8 percent

respectively.2 Guaranteed access to chips, especially advanced semiconductor

chips is becoming a key policy goal when assessing national security and

economic competitiveness to counteract sudden disruptions to supplies.

In the past

decades, typhoon, earthquakes, infrastructure shutdown due to power shortage or

fires at the manufacturing sites, were the major causes for supply disruption.3

While in recent years, escalating geopolitical tensions and governments’

counter-measures, including potential military conflicts, trade sanctions and

stringent export control mechanisms, may threaten supply chains more than

traditional risks.4

Yet an over

simplified approach to examine who needs what in the complicated semiconductor

world overlooks business reality of the trillions dollar supply chains and the

deep interdependence between players in the eco-system. There are different

layers (sub-sectors) of the semiconductor supply chains, including IC design,

materials, equipment and tools, and manufacturing, the latter includes wafer

fabrication, assembly, packaging and testing (APT).5 The United States, Europe

and Japan dominate IC design, materials, equipment and tools, while East Asia,

mainly Taiwan, South Korea and China, take the lion’s share of manufacturing.

In the interdependence relations, IC design houses and Integrated Device Manufacturers

(IDMs)6 in the United States and Europe contract manufacturing to specialized

manufacturers, including fabrications (Fabs), Outsourced Assembly and Test

(OSAT), in East Asia for mass production. On the other hand, East Asia depends

on R&D, IP, equipment and tools provided by the United States and Europe

for their manufacturing activities, they also need Japan and a handful of other

countries to provide critical materials such as photoresist, specialty

chemicals and the materials needed for manufacturing. For example, in the

aftermath of Russian invasion in Ukraine in February 2022, possible supply

disruption of Neon from Ukraine threatens the semiconductor industry.7

Geographical

specialization is key to technological advancement and cost efficiency which

have enabled strong growth of the semiconductor industry for two decades. The

clustering effects also led to over concentration of the supply chains, in

particular the manufacturing activities, in only a few countries. According to

Semiconductor Industry Association (SIA), in 2019, not only more than 75

percent of chips were manufactured in East Asia, more than 82 percent of them

were assembled, packaged and tested in the same region, too. Around three

quarters of semiconductor manufacturing capacity is located in China, Taiwan,

South Korea, and some in Singapore and Malaysia. However, what was regarded as

the most cost effective business models was re-assessed in the aftermath of the

semiconductor shortages since 2020. The overdependence on East Asia becomes a

dangerous sign to national security as geopolitical tension in East Asia

continues to escalate.

Furthermore,

according to SIA, for all of the world’s manufacturing capacity of chips in

nodes below 10 nanometers (10 nm), currently the most advanced technology, 92

percent is located in Taiwan, while 2 percent is located South Korea. Although

only 2 percent of the global capacity is on nodes below 10 nm today, these advanced

chips are widely used and will have the fastest growth. It will impact almost

all strategic technology industries if supply disruption happens.

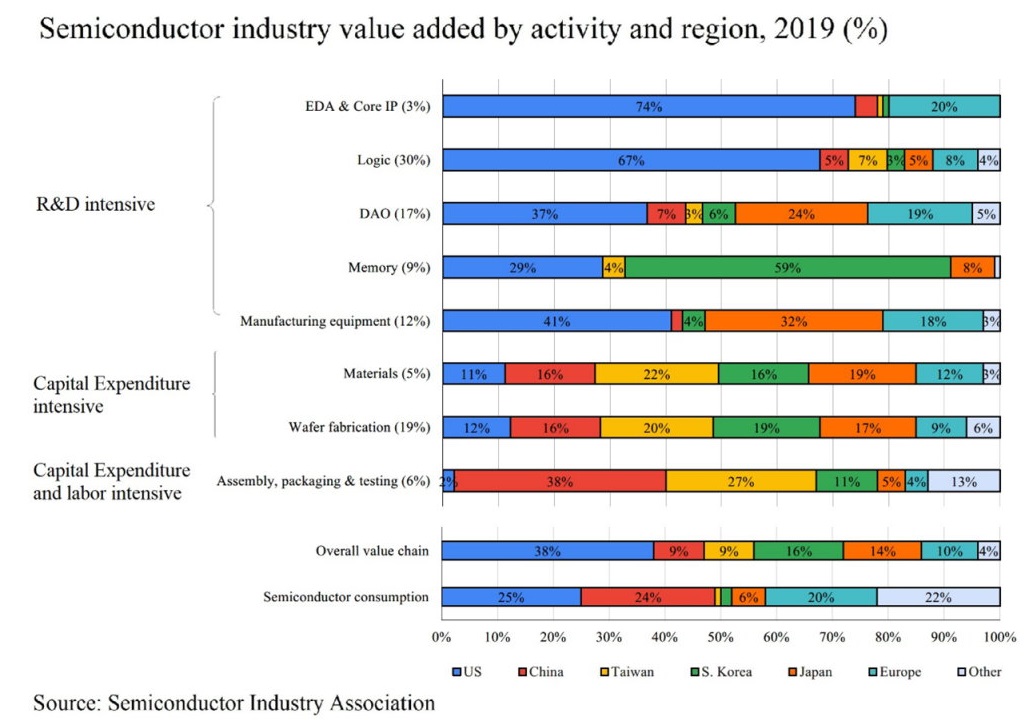

Figure 1: Sub-sectors of semiconductor industry by

region (2019

Among the

different layers or sub-sectors of manufacturing of semiconductor, the wafer

fabrication (front-end manufacturing) is the most technology- and capital-

intensive, making it very difficult, and expensive, to have new competitors in

the short term. It also requires strong supports from the public and private

sector to share capital expenditure and R&D costs. And while the stage of

APT (back-end manufacturing) requires much less technology and capital

intensity than the wafer fabrication, it nevertheless is still highly

specialized. As fabrication technology improves, advanced packaging and testing

also becomes more technology-intensive.

Another feature is

labor intensity required at the production sites. Taiwanese manufacturers had

been relocating APT capacities to China since the late 1990s to take advantage

of its abundant labor force and low labor cost. Since then, China has emerged

as the world leader with its share in value added in global APT supply rising

to 38 percent, while Taiwan is now ranked second with a share of 33 percent.

Taiwan’s focus is more in advanced packaging.8 Some developing countries are

also participating in the sub-sector, such as Malaysia, Philippines, Thailand

and Vietnam in Southeast Asia. Under the current trends of diversification of

semiconductor supply chains, these countries are competitive in their young

labor force and comparatively lower labour cost than China. When considering

geopolitical tensions in the region, these countries also have lower

geopolitical risks.

The manufacturing

activities, from fabrication to APT, are the United States’ greatest weaknesses

in the whole semiconductor supply chains. In 2019, U.S. share of global

fabrication, and assembly, packaging and testing was 12 percent and 2 percent

respectively. SIA estimates that the country will need to invest an extra total

of $350 to $420 billion in manufacturing capacity in order to establish the

complete semiconductor supply chains in the United States and may be able to

reach the goal of self-sufficiency.

State of Play of in Taiwan’s Semiconductor

Industry

Taiwan started

developing its chip sector in late 1970s, when the government tried to promote

a transformation of vertical integration of its consumer electronics

manufacturing activities so semiconductors could be domestically sourced. The

goal was to localize manufacturing of semiconductors and the equipment and

devices needed in order to support its consumer electronics industry, with the

semiconductor industry in Taiwan becoming a catalyzer to boost electronics

industries, instrumental to Taiwan’s leadership positions in Information,

Communication and Technology (ICT) and electronics industries. Concentrating on

contract manufacturing, or Original Equipment Manufacturing (OEM) and Original

Design Manufacturing (ODM) for international brand clients, Taiwan has been the

world’s largest manufacturer of smartphones, laptop computers, printed circuit

boards, data center servers, and dozens of other products.

The similar ODM

mode was applied when Taiwan started its semiconductor industry. Taiwan

Semiconductor Manufacturing Company Limited (TSMC), the most important and

largest fabrication in Taiwan and in the world, and other fabrications in

Taiwan, adopted the contract manufacturing model to provide manufacturing

services (“foundry”) for the United States and Japanese semiconductor companies

without semiconductor fabrication factories (fabless). Contract manufacturing

allowed the fabless companies concentrate on research and design. Gradually,

Integrated Device Manufacturers (IDMs)9 including Intel and Micron in the

United States, Japan and Europe also began to rely on Taiwan contract

manufacturers for a portion of their manufacturing needs. This business model

has become the backbone of semiconductor manufacturing in Taiwan. It has also

helped develop IC design and back-end (or downstream) manufacturing of APT in

Taiwan.

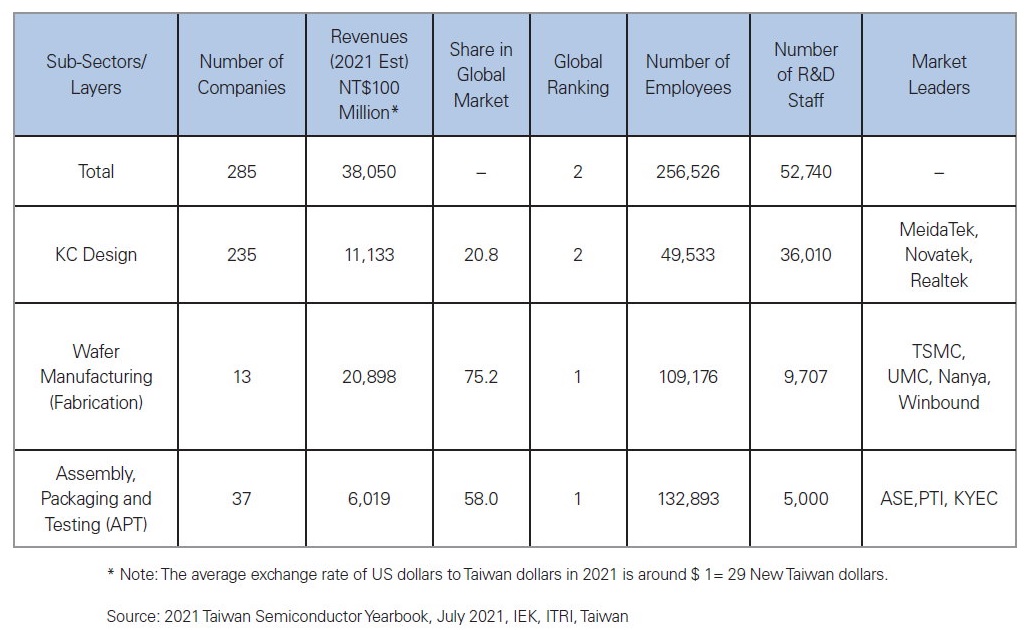

Table 1: Major Sub-sectors/Layers of Semiconductor

Industry in Taiwan (2021e)

Given its small

domestic market, the industry has targeted international markets since the

beginning. In 1990s and 2000s, Japan, the United States and Europe together

represented around 40 percent of the export market, while since 2000s, exports

to China and Southeast Asia quickly picked up, indicating a shift of the

semiconductor supply chains moving towards Asia.

According to the

Industrial Technology Research Institute (ITRI) of Taiwan, as of 2021, the

United States was Taiwan’s largest client, accounting for 40 percent of total

revenue, followed by China, accounting for 28 percent. By sub-sectors, China

accounted for more than 50 percent of Taiwan’s IC design revenue, while the

United States was the largest client for both wafer fabrication and APT. The

share was 54 percent and 50 percent respectively.10 These figures suggest that

Taiwan has developed separate and different business relations with the United

States and China, its two largest clients. Taiwan serves for IC design firms

and IDMs in the United States by providing manufacturing capacity, while

provides IC design and contract manufacturing to Chinese clients for matured or

commodity chips and commercial end-use applications. These clearly defined

separation systems allow TSMC and other leading companies in the semiconductor

supply chains continue to be their U.S. clients’ trusted partners and

suppliers.

The key to the

success of Taiwan’s semiconductor industry is the ability to manufacture

efficiently and cost-effectively with the highest quality/yields in the world.

According to TSMC, Taiwan has developed a dynamic ecosystem that provides

infrastructure, know-how, human talents, and close relations with both Western

and Asian clients. Most of all, Taiwan is also home to the ICT and electronics

manufacturing activities, where products embedded with the semiconductors are

assembled and shipped to international market. This unique model of vertical

integration of semiconductors and applied industries is the back bone to

Taiwan’s dominant position in both the semiconductor and electronics supply

chains.

East Asia is

currently the largest integrated manufacturing hub for electronic devices,

together manufacturing more than 60 percent of the global supply of consumer

electronics, smartphones, and PCs. The clustering effects increase benefits of

geographical proximity of the hub to Taiwan –as well as within Taiwan- in

shipping components to be assembled into devices. However, to mitigate risks of

geographical concentration, the ICT and electronics supply chains are also

facing pressing needs for diversification.

The Taiwanese

government too has key role in guiding and managing the development of Taiwan’s

core technology in the semiconductor industry in the past 2 decades. As a

result, despite close business ties across the Taiwan Strait, Taiwan’s

semiconductor industry continues to keep its manufacturing facilities and

R&D functions at home. As of 2021, nearly 95 percent of Taiwan’s

manufacturing capacity is located in the island. Only 3.5 percent of capacity

is placed in China and 1.7 percent in other regions. This is partly attributed

by a very stringent outbound investment screening mechanism adopted for China.

Currently only 200 mm (8 inch) and 300 mm (12 inch) wafer fabrications are

allowed for investments in China, meaning all investments of advanced

manufacturing in China are prohibited.11 Furthermore, for national security and

the need to maintain competitiveness, Taiwan recently passed amended National

Security Law to create a new clause to regulate act of economic espionage,

particular the adversary force in China, Hong Kong and Macao.

The United States Needs a Longer Term Supply

Chains Strategy

To respond to U.S.

government’s call to increase self- sufficiency of strategic products and to

benefit from a series of U.S. investment incentives, the semiconductor industry

has recently announced approximate $80 billion new investments in the United

States during 2021 through 2025, according to SIA. These investments will not

only create tens of thousands of good paying jobs in the United States, but

will also secure U.S. role in the global semiconductor supply chains.12

In 2021, the

global semiconductor market reached $430 billion, and is estimated to increase

to $772.03 billion by 2030 at a compound annual growth rate (CAGR) of 6.6

percent from 2021 to 2030.13

Since Congress

passed the Creating Helpful Incentives to Produce Semiconductors (CHIPS) for

America Act in January 2021, foreign corporate interest to invest in chips has

expanded as well. TSMC announced a $12 billion project, Samsung will invest $17

billion factory in Texas, and SK Group will develop a R&D center. In

addition, ASML of the Netherlands will spend $200 million to expand its

facility in Wilton, Connecticut. The project aims to support fabrication of

advanced chips in the United States

U.S. companies too

are also getting ready to reshore manufacturing. Intel plans to invest $20

billion facility in Ohio, Texas Instrument will spend $30 billion in Texas,

Cree is planning a $1 billion expansion of its factory in North Carolina, and

Micron plans to expand U.S. production too.14

Investing in new foundries

is critical to enhance long-term resilience of the semiconductor supply chains

in the United States However, shifting or relocating supply chains may reduce

productivity and decrease profitability. It may also lead to overcapacity in

chip making. So while new investments could reduce supply chain bottlenecks,

the White House needs to develop a longer term supply chain strategy that is

flexible and commercially viable.

In fact, Asia is

increasingly worried of a possible slowdown in the semiconductor industry,

including overinvestment in fabrication. A downturn is already being felt in

Taiwan and South Korea, and if global demand continues to weaken, further

worsened by growing inflation in almost all major economies, investors may

reconsider and postpone their investment plans. This will post uncertainty to

the development of supply chains in the United States

Meanwhile, state

subsidies and other government initiatives have their limits. The CHIPS and

Science Act establishes investments and incentives to support U.S.

semiconductor manufacturing, research and development, and supply chain

security. The Act will provide $52 billion to manufacturers in the

semiconductor industry located in the United States and an income tax credit of

25 percent. It will also subsidize semiconductor equipment, materials or other

manufacturing facility investment through 2026.

The SIA estimates

that the $50 billion incentive program would enable the construction of around

19 fabrications in the United States, and that the cost for building an

advanced fabrication in the United States ranges from $10 billion to $20

billion. Considering it would cost at least $10 billion to build the factory in

Taiwan, the cost in the United States may even double or triple, taking into account

the high inflation and difficulty to source necessary materials locally. Thus,

the state subsidies under the CHIPS and Science Act may only partially cover

the investors’ capital expenditures. The U.S. government will need to consider

any other subsequent funds to support continuous investments if the money runs

out. The government will also need to address decades of underinvestment in the

country’s infrastructure, workforce, small businesses and rural economies.

Large companies

such as TSMC may be able to self-fund fab construction through the equity and

debt markets, but small business and startups will need financial support from

the government and private sector.

Workforce

development is another challenge. TSMC has expressed concerns about recruiting

talent including operators, technicians and engineers in the United States. It

should be noted that the corporate culture of Taiwan and South Korea require

full commitment and rigid discipline at the workplace. For instance, most

Taiwan semiconductor companies very often arrange two shifts of workers a day

to fully utilize their manufacturing capacities. Such practices at workplace is

not usual in the United States.

At the same time,

even in an industry that is automated over 99 percent, highly educated staff

are needed to handle the complexity of advanced technology, and a large talent

pool of different education levels. Yet the United States has had a talent

shortfall partly because of decades-long under-investment in university

programs.15 The fight for talents will soon arise if the United States, Japan,

South Korea, and Taiwan fail to well prepare themselves for developing a new

generation of talents in technology industries.

The

Science/Research Act will allocate around a total of US $250 billion in the

R&D and talents development, which will provide a significant boost to US

industry. U.S. educators will need to promote awareness and interests in the

manufacturing activities given U.S. university graduates still tend to focus on

the IC design and startups in the industry rather than working in factories.

Failure to address the challenges of creating sufficient, skilled human talent

in the United States will undermine the highly expected job-creation function

of the semiconductor industry in the country.

A recent survey of

the non-government semiconductor association SEMI of U.S. member companies indicates that more than 5 percent

of engineering positions are presently unfilled. This suggests that that the

U.S. higher education system currently does not supply enough fresh talent to the semiconductor industry.

SEMI estimated that the U.S. microelectronics workforce development (WFD) needs

will more than double as CHIPS Act programs create tens of thousands of new

jobs.16 The need for highly skilled engineers and technicians in the next few

years will be a challenging issue for both the investors and the state

governments hosting the investments.

Taiwan’s Response to U.S. Supply Chains

Resilience Initiatives

Taiwan is a

leading investor in manufacturing industries in East Asia with footprints

across China, Southeast and South Asia. Since U.S. - China trade frictions

escalated in 2017, Taiwan has adopted strategies to mitigate increasing risks

of its investments in China. Taipei has adopted a series of investment

incentives to encourage reshoring back to Taiwan or diversification of

investments away from China. Programs include the “Return to Taiwan” package17

and the New Southbound Policy (NSP) for promoting closed economic ties with

selected Southeast or South Asian countries.18 Taiwanese companies have looked

to relocate or expand facilities in neighboring Asian countries, most notably

Vietnam and India. Some are also considering reshoring to the United States or

nearshoring to Mexico and other Latin American countries. Taiwanese investments

in Vietnam, India, the United States and Mexico have increased considerably

over the past several years.

The 2020 New

Southbound Policy has promoted further business ties between Taiwan and main

Southeast Asian partners, including Vietnam, Thailand, Malaysia, Philippines,

Indonesia and Myanmar, in the aftermath of U.S.-China trade conflicts and

COIVD-19 pandemic. Vietnam, Thailand, Indonesia, and Malaysia have become

particularly attractive for consumer electronics supply chains. Vietnam,

Taiwan’s largest FDI destination in Southeast Asia, has benefitted from

relocation of the Apple supply chains, thanks to increasing Taiwan contract

manufacturers of Apple products investing in north Vietnam. According to the

Taiwan Representative Office in Vietnam, accumulated FDI from Taiwan in Vietnam

amounted to $80 billion to $100 billion, creating 1.5 million jobs in the

emerging Asian factory.

Another reason for

Taiwan’s continuous investments in the region is the accelerating economic

integration in the regional and with global markets, most notably the CPTPP.

Integrated market opportunities and preferential treatments these mega FTAs

provide keep attracting Taiwan investments.

Taiwan’s

investment in the United States showed strong growth momentum. In 2020,

registered Taiwan capital outflows to the United States amounted to $4 billion,

making the United States the second largest destination for Taiwan capital

outflows, only next to China.19 The changing pattern of investment decisions of

Taiwan companies reflects a growing interest in relocating supply chains

directly in the destination markets, bringing potential paradigm shift in

Taiwan-U.S. economic relations.

U.S. technology

companies are also expanding their operations in Taiwan since 2015. Google,

Yahoo, Micron, Applied Materials, Microsoft, Facebook, and Apple have

established data centers, R&D centers, and AI centers in Taiwan. Micron and

Applied Materials also continue to expand manufacturing facilities in Taiwan.

Given US-Taiwan

economic partnership being highlighted by both governments, there is ample

potentials for the two sides to work together on semiconductor supply chains in

the U.S. TSMC’s $12 billion project in Arizona is one such case. In May 2020,

TSMC announced its intention to build an advanced semiconductor fab in Arizona.

The facility will utilize TSMC’s 5 nm technology for semiconductor wafer

fabrication, with a 20,000 semiconductor wafer per month capacity, and create

over 1,600 high-tech professional jobs. Construction started in 2021 with

production expected to begin in early 2024.

TSMC’s total

capital expenditure approximately reached $12 billion from 2021 to 2029. The

reasons for the investment are to better support U.S. customers and partners

and to attract global talents. TSMC also has a fab in Camas, Washington and

design centers in both Austin, Texas and San Jose, California. The Arizona

facility is TSMC’s second manufacturing site in the United States20

What is no less

noteworthy is the recent investment project of GlobalWafers to build a

state-of-the-art 300-millimeter silicon wafer factory in Sherman, Texas.21

GlobalWafers is Taiwan’s largest and world’s third-largest wafer manufacturer

providing wafers as materials for fabrication. According to the company, the

3.2 million-square-foot factory will support around 1,500 jobs with production

volumes reaching 1.2 million wafers per month, estimated to start in early 2025.

The new factory is

the largest advanced silicon wafer manufacturing facility in the United States

over two decades. According to GlobalWafers USA (GWA), the production will

support advanced fabrications in the U.S. GWA’s factory signals the beginning

of 300-millimeter silicon wafer fabrication in the United States, filling

another “gap” of U.S. efforts to develop a complete semiconductor eco-system in

the country.

Meanwhile,

MediaTek, the world’s 2nd largest IC design company based in Taiwan, signed

into an MOU with Purdue University in June 2022. The University’s College of

Engineering will open MediaTek’s first semiconductor chip design center to

research on next-generation computing and communications chip design. In May,

the university also announced the launch of its Semiconductor Degrees Program,

a comprehensive set of innovative, interdisciplinary degrees and credentials in

semiconductors and microelectronics. MediaTek has been working with U.S.

universities for more than a decade. The project will also include a new

MediaTek design team right on campus.

These three

projects reflect Taiwan’s commitment to work together with the United States

across the semiconductor supply chains. If these investments are implemented

smoothly, they will bring a new era of Taiwan-U.S. strategic economic

partnership stronger than ever for jointly tackling challenges in current

global economic context.

It should be

noted, though, that Taiwan’s success in key manufacturing industries, including

semiconductors, is the ability to create an ecosystem with integrated

manufacturing activities from upstream (such as materials, equipment, R&D)

to middle and downstream (such as components, assembly), making the most of the

clustering effects. Therefore, TSMC’s success in Arizona will lie in the

clustering effects it can bring to support fabrication. One challenge is that

TSMC needs strong supports of its key suppliers to provide on-site

construction, logistics, components, materials and all critical services.

However, as most of the key suppliers are small and medium sized companies in

Taiwan, they are not eligible to state subsidies under the CHIPs Act or other related

programs. Some of them are already having difficulties setting up U.S.

subsidiaries or recruiting local skilled workers. Biden administration should

come up with programs to assist these smaller key suppliers if the United

States wishes to maximize the clustering effects of TSMC’s project.22

The Limits of the State Subsidies

The U.S.-led IPEF

trade framework highlights the need to establish a resilient supply chain that

goes beyond relocation of supply chains and attracting investments to the

United States, including having a skilled workforce, improved infrastructure,

logistical efficiency, healthy business environment and support from both the

public and private sectors.

Supply chain

disruptions have been a major challenge to both Trump and Biden administrations.

The current disruptions challenge initially referred to the disorders in global

supply since President Trump first imposed 301 tariffs on Chinese imports in

July 2020. The disruption was further broadened during the COVID-19 pandemic,

and came to hit the U.S. economy most when the global shortage of chips started

to affect global production and sales of automobiles and other sectors and

stressed U.S. imports, exports, and the movement of goods nationwide.

To address the

supply chains vulnerability issues, Biden administration had passed

legislations include Defense Production Act, the U.S. Innovation and

Competition Act (USICA) and the CHIPS for America Act. The Defense Production

Act allows the U.S. Department of Defense use authorities to strengthen supply

chains for key defense-related semiconductors, while the USICA mandates full

funding to catalyze more private-sector investments and continued American

technological leadership.

To address the

semiconductor supply chains resilience, there are currently various mechanisms

in Biden administration, such as the U.S.-EU Trade and Technology Council

(TTC), the U.S.- Japan initiative, IPEF, and some other initiatives already

proposed or in shaping.

The Trade and

Technology Council was launched at the U.S.-EU Summit in June 2021. The United

States and EU intend to enhance cooperation on measures to advance transparency

and communication in the semiconductor supply chain and identify gaps, shared

vulnerabilities, and opportunities to strengthen their domestic semiconductor

R&D and manufacturing ecosystems to improve resilience in the supply chain.

They also agreed to enhance cooperation on issues related to investment

screening and export controls. 23

Biden

administration and Japanese government launched a U.S.-Japan Competitiveness

and Resilience (CoRe) Partnership in April 2021. Both agreed to enhanced

cooperation on semiconductor manufacturing capacity, diversification,

next-generation semiconductor research and development, and responding to supply

shortages. Further collaborations were announced after Prime Minister Kishida

Fumio of Japan took office, which included joint action to develop, among

others, 2 nm advanced chips under bilateral efforts.

Another new

mechanism is the U.S. led CHIP 4, or Fab 4 initiative, which is proposed by the

United States, reportedly as a working level platform for exchanging market

information and handling operational issues. The CHIP 4 initiative will include

the United States, Japan, South Korea and Taiwan. However, according to Korean

media, South Korea expressed concerns that the group may develop into an

anti-China mechanism, which may threaten Samsung’s and SK’s huge investments in

China. The initiative also raises questions such as its overlapping purpose and

functions, and how it may fit into the supply chains strategy. South Korea’s

concerns reflect its difficult situation, so are some other Asian countries, in

not supporting economic decoupling and taking sides between the world’s two

largest economies.

Besides

collaboration with Europe and Asia, President Biden also announced the launch

of the Americas Partnership for Economic Prosperity in early June, a historic

new agreement when Biden hosted the Summit of the Americas on June 8th, where

he also prioritized collaboration with the Latin American and the Caribbean

nations on making more resilient supply chains.24

The aforementioned

supply chains mechanisms, large or small, has different membership but similar

purpose. However, the fragmented and overlapping mechanisms and varying working

agendas with different countries or partners make them confusing and may hinder

the U.S.’s efforts to develop a holistic and cross-cutting strategy and develop

concrete work programs.

For example, the

EU dominates supply of semiconductor equipment and tools for manufacturing, but

none of the existing semiconductor initiatives invite both EU and Asian

partners. Moreover, though President Biden’s Indo Pacific Strategy released in

February include Latin America countries such as Mexico, Chile and Peru, but

none of them were invited to the IPEF. Instead, President Biden launched the

Americas Partnership for Economic Prosperity to address supply chains solely

with the Latin American countries.

Last but not

least, Taiwan was also not invited to the IPEF or other existing semiconductor

supply chains initiatives, except for the CHIP 4. This further sends a

confusing message to Taiwan and the world.25 Though Biden administration

launched a bilateral initiative – the Taiwan-U.S. Initiative on 21st Century

Trade - after IPEF was launched, Taiwan is still denied from access to

information sharing with other stakeholders in the semiconductor supply chains

and engagement with them. Keeping important players or potential new comers away

from the semiconductor supply chains initiatives may hinder the efforts to

integrate the whole supply chains and handle common concerns and interests,

such as investment policy and international standard setting issues.

Risks of State Subsidy Competition

On August 9,

President Biden signed into law the CHIPS and Science Act, which will provide

$52 billion to catalyze investments in semiconductor industry in the United

States The passage of the Act demonstrated bipartisan support for reengaging

semiconductor supply chains in the United States to address chip shortage,

create good-paying jobs and maintain leadership in technology. Among the $52

billion, $39 billion will be used to fund manufacturing facilities either by

foreign or U.S. companies. The Biden administration expects the funding can

attract leaders in the supply chains to set up new investment or expand

existing ones in the country.

Because costs to

manufacture advanced semiconductors are much greater in the United States,

Europe and Japan than in Taiwan or other Southeast Asia, governments have to

provide subsidies to attract leading companies to build manufacturing

facilities in their countries. Huge state subsidies from wealthy countries have

already triggered a race for subsidies and competing for potential investors.

This may further contribute to inflation.

For example, the

EU plays a key role in advanced IP design, key semiconductor equipment and

tools and wafer raw materials, but it lacks semiconductor manufacturing, same

as the United States, and has little capacity for APT. In December 2020, the EU

released a Joint Declaration on Processors and Semiconductor Technologies with

an aim to bolster Europe’s electronics and embedded systems of value chains.

The EU Commission President Ursula von der Leyen also introduced the European

Chip Act, with a goal to double its share of global semiconductor production

from currently around 9 percent to 20 percent by 2030, and to 25 percent beyond

2030. EU governments and the private sector will invest more than 43 billion

euros to develop semiconductor supply chains. More than two-thirds of the

budget will be in the form of state grants to encourage manufacturers to build

new cutting-edge wafer factories or mega fabrications.

According to a

chips survey in EU released in February 2022, chip demand is expected to double

between 2022 and 2030, with significant growth in the future for leading-edge

semiconductor technologies. It also found companies establishing new chip

fabrication facilities consider finding qualified labour and compliance with

government regulations key issues when they select manufacturing locations.

In Asia, Japan

also announced in mid-2021 that it will provide $8 billion in state funds to

supplement its semiconductor industry. In July 2022, Japanese Diet passed the

legislation to provide subsidies to private sector investment in semiconductor

industry. TSMC became the first foreign investor to be granted with $3.5

billion to subsidize its fabrication factory in Kumamoto which will produce 28

nm chips for its client Sony company. In May 2021, South Korea also announced a

policy to support semiconductor industry with $450 billion in tax credits

through 2030 for private domestic companies to invest in R&D and

manufacturing.

The United States,

Europe, Japan and South Korea, and a number of other countries, all set up

their government policy to establish self-sufficient semiconductor supply

chains and are ready to provide generous state subsidies to attract

investments. According to SEMI, there will be more than 30 wafer fabrications

to be built worldwide between 2022 to 2024, which means an extra amount of more

than 30 percent of manufacturing capacity will be added to global supply.

However, these

programs and state subsidies may create risks of over-capacity, as increasing

worries in the global market are already observed for potential market

protectionism and geo economic-political conflicts that will add to business

operation costs and create unexpected loss.

Very few U.S. chip

manufacturing investments are in the assembly, packaging and testing

sub-sector. Korea’s NAND Flash SK Hynex is one of the few that recently

announced its investment plan to build an advanced testing and packaging

factory in the United States, scheduled to start building in early next year

and start quantity production in 2025-2026. The investment projects, amounting

to $22 billion, will include semiconductors, green energy and biotechnology,

with around $15 billion in semiconductors. SK plans to apply for subsidy of the

CHIPs Act, making it one of the few companies already announced to build

testing and packaging capacities in the United States since the CHIPs Act was

introduced.

The relatively

less skill- and capital-intensive nature of packaging and testing was dominated

by East Asia, accounting for more than 80 percent of global supply. China is

building dozens of new factories for advanced packaging and testing in the

aftermath of the COVID-19 pandemic. The United States needs to think hard how

its strategy to encourage relocation of assembly, packaging and testing into

the country.

Why packaging and

testing industry is more difficult than fabrication to relocate in the United

States? The key reason is labor costs and labor issues. For instance, Taiwan

currently has 37 manufacturers in assembly, packaging and testing, altogether

hiring more than 130,000 workers. Comparatively, wafer fabrication in Taiwan

has three times of annual revenues than assembly, packaging and testing, but

hire only around 100,000 workers (including engineers and operators). Taiwanese

companies had since the 1990s outsourced most of manufacturing to China and

other Southeast Asian countries, contributing to relocation of the

semiconductor supply chains in these countries. As of today, Taiwan continues

to dominate advanced packaging and testing, while has shifted most matured

packaging and testing to China and Southeast Asia.

Most APT companies

would not consider it commercially viable to move APT facilities in the United

States due to difficulty to hire workers and stringent labour laws and

practices. For example, the ASE Technology Holding Co (ASEH) in Taiwan, the

world’s largest packaging and testing company, employs around 80,000 workers in

Taiwan, with around 5 percent foreign workers. Furthermore, workers in the

packaging and testing factory take two shifts, sometimes three shifts, in the

factory. This would be violating labour laws or regulations in many states in

the U.S. It is very likely that in the next few years, after new fabrications

begin operation in the U.S., companies would still need to outsource packaging

and testing to East Asia, and ship the finished products back to the United

States or other destinations for further process. This may appear to hinder the

supply chains resilience as a critical part of the manufacturing does not take

place in the United States, but this may be a more commercially reasonable outcome.

Promoting International Collaboration

The IPEF and other

initiatives highlight the importance to work with like-minded partners to

improve the supply chains resilience. The U.S. strategy has prioritized

transferring of supply chains back to the United States or closer to home, but

when both are not commercially viable, working with like-minded partners

through “friend-shoring” can ensure supply chains will be relocated to trusted

and friendly countries. Under the concept of “friend-shoring”, it is important

to identify who are the friends and what kind of roles these friends could

play. The often mentioned friends are Vietnam, Malaysia, India, Mexico, Cost

Rica and several other Latin American countries. The United States can work

with these countries to establish less technology intensive capacities, such as

APT. However, to enable these potential new comers participate in the

semiconductor industry, some of them are already building small capacity. The

United States needs to provide capacity building and promote international

collaboration with stakeholders in these countries.

Since the 1980s,

Taiwanese companies have established comprehensive business networks and

manufacturing facilities in Southeast and South Asia, ranking among the top

foreign investors, especially in manufacturing sectors, including textile and

garment, footwear, electronics and ICT products.26 Taiwan companies, as

contract manufacturers, U.S. clients or importers, and a Southeast Asian host

country, have developed vital triangular cooperation. For example, U.S. clients

invite contract manufacturers of Taiwan companies to establish facilities in a

Southeast Asian country, Mexico or Honduras, place orders to them to contract

manufacturing Polo shirts, Nike sneakers, or iPads for the U.S. market.

In the past

decades, this triangular partnership has not only boosted U.S.-oriented supply

chains in countries such as Vietnam and Mexico, but also has helped the United

States to diversify import sources. For example, since the U.S.- China trade

conflicts escalated in 2018, Taiwan electronics companies also significantly

expanded manufacturing facilities in Vietnam and Mexico, exporting from these

two countries assembled products to the U.S. market to avoid the 301 tariffs

imposed on Chinese products and further geopolitical tensions. Taiwan-invested

supply chains in Southeast Asia and Latin American countries can further

contribute to the “friend-shoring” or relocation of semiconductor supply chains

in these areas.27

A timely example

is Apple requesting its key suppliers, mostly large Taiwanese electronics

companies, to set up facilities in Vietnam and India to diversify Apple’s

import sourcing. Taiwanese companies have expanded footprints in Vietnam and

India, bringing these two new comers into the Apple supply chains.28 Taiwan is

already among the largest foreign direct investors in Vietnam and Mexico. Total

Taiwan FDI in Vietnam amounts to $50 billion, recent growth focusing in ICT and

electronics industries by large Taiwan companies to serve their U.S. clients.

Vietnam works closely with Taiwan investors in its strategic industrial plans.

Taiwan investment in Mexico also significantly increased in ICT industry.

Taiwan has fabrications in Singapore, has packaging and testing facilities in

Malaysia and Philippines. The semiconductor industry can be another area for

the United States, Taiwan, Vietnam, or Malaysia, or Mexico trilateral

collaboration. Taiwan can bring capacity building in collaboration with the

United States to these countries, share experiences in developing semiconductor

industry and help design training programs.

Conclusion and Policy Implications

Building

manageable, resilient and self-sufficient semiconductor supply chains to reduce

over dependence in East Asia is a priority for the United States IPEF and the

CHIP 4 Alliance reflect U.S. strategy towards establishing resilient

semiconductor supply chains on U.S. soil. The efforts have significantly

progressed with the passage of the CHIP Act and announcement of major

investments in the United States In particular, the announcement of TSMC to

build a fabrication factory on 5 nm in Arizona marks the beginning of reshoring

of the supply chains back to the United States

However, the Biden

administration’s strategy does not address key issues. The emergence of a

subsidies race among industrialized countries to build their own supply chains,

fragmented mechanisms to integrate stakeholders in the supply chains,

difficulties of fabrications to recruit a skilled workforce, the lack of APT

facilities in the United States are but a few of challenges that have been

neglected by the White House to date. At the same time, there is declining

global demand and risks of overcapacity in chip production.

Furthermore, Taiwan’s

potential role to address the looming supply chain challenges is underrated.

Neither is Taiwan’s participation in the supply chains could hugely contribute

to the U.S. strategy as is expected. The risks of underestimating Taiwan’s role

is considerable, and there are looming risks to Washington’s semiconductor

supply chain resilience strategy as it currently stands.

First of all, the

over politicization of supply chains issues may hinder construction and

operations of the semiconductor supply chains. Certainly, Southeast Asia and

other participating countries have concerns that IPEF may have become overly

politicized.29 Some countries also suggest that the IPEF and CHIP 4 initiative

should be inclusive and welcome all players in the supply chains. Therefore,

inviting Taiwan to join IPEF and other relevant initiatives and alliances can

strengthen supply chains. The United States also needs to demonstrate its

leadership to integrate Indo Pacific like-minded partners, including Taiwan and

Southeast and South Asia, in its supply chains strategy. As the United States

has explicitly demonstrated its commitments to security of Taiwan Strait, it

should also publicly support Taiwan’s economic security by incorporating Taiwan

into its major multilateral economic and industrial strategy, including in the

semiconductor industry.

Second, it is

estimated that 42,000 new jobs will be directly created by CHIPS Act in the

future. The United States should develop joint programs with Taiwan for

training skilled workforce and talents. It is estimated that more than 5

percent of engineering positions are presently unfilled, and that the need for

microelectronics workforce in the United States will double, mostly highly

skilled engineer and technician roles, in the next few years. Taiwan has over

three decades of experiences of cultivating human resources to meet the need of

the semiconductor and electronics industries in Taiwan. The United States and

Taiwan should develop joint programs to improve supply of university graduates

from the U.S. higher education system. The programs should also provide

preparatory and on-site training to workforce in the semiconductor supply

chains located in the United States30

Third, the

semiconductor supply chains encompass IC design, materials, equipment and

tools, fabrication, and APT. The United States is a leader in IC design and

equipment and tools, but lags far behind Asian countries in fabrication and

APT. The CHIPS Act helps attract investments of TSMC, Samsung, SK, Intel, and

other major companies. However, when these fabrications begin operation, the

fabricated chips will need to be shipped back to Asia for assembly, packaging

and testing, due to little APT capacity and no advanced packaging and testing

at all in the United States Taiwan is the world’s largest player in APT,

particular focusing advanced testing. The United States should work with Taiwan

to encourage Taiwan investments of this sub-sector in the United States by

providing assistance to address the need of intensive labor force, and access

to financial and other supports in the United States The United States should

also collaborate with TSMC to solve challenges facing its key suppliers in

supporting TSMC operation in Arizona.

Fourth, the United

States should work with Taiwan to provide capacity building to Southeast Asia

and Latin America countries, including Vietnam, Malaysia, and Mexico. Taiwan

has long developed electronics clusters in those countries. A trilateral

collaboration has existed in these industries for decades, namely Taiwan

contract manufacturers manufacture products in Southeast Asia or Mexico for

exports to the U.S. market. The trilateral collaboration model can be

duplicated or expanded in the semiconductor supply chains in Vietnam or Mexico

through more policy dialogues among three parties, such as through

“friend-shoring” initiatives to outsource APT activities in these countries.

Written by Kristy

Tsun Tzu Hsu

Published in

Wilson Center, Sep 28, 2022

For more

information, please see https://www.wilsoncenter.org/event/taiwans-role-us-semiconductor-supply-chain-network

________________________________

Kristy Tsun Tzu

Hsu is the Director of the Taiwan ASEAN Studies Center (TASC) at Chung Hua

Institution for Economic Research (CIER), Taiwan, and she was a visiting fellow

at the Woodrow Wilson Center in the U.S. in July-August, 2022.

Endnotes

1.

The

Administration released findings from the comprehensive 100-day supply chain

assessments for four critical products (semiconductor manufacturing and

advanced packaging; large capacity batteries; critical minerals and materials;

and pharmaceuticals and active pharmaceutical ingredients).

2.

Boston

Consulting Group, SIA. (2021), Strengthening the global semiconductor supply

chain in an uncertain era.

https://web-assets.bcg.com/9d/64/367c63094411b6e9e1407bec0dcc/bcgxsia-strengthening-the-global-semiconductor-value-chain-april-2021.pdf

3.

For

example, in 1999, a strong earthquake in the center of Taiwan caused a week

long shutdown of the semiconductor companies in Hsinchu Science Park as a

result of power outages. The memory-chip prices soon tripled which impacted the

global market. Many large companies outsourced manufacturing to Taiwan suffered

huge loss.

4.

Before

the U.S.- China rivalry, in 2019, Japan imposed export controls on

semiconductor materials to South Korea, causing huge loss for South Korea. The

sanctions on Russia after its invasion in Ukraine in February 2022 also

threatens disruption of semiconductor materials. Apart from these, increasing

tensions in the Taiwan Strait also raises global concerns on possible disrupted

supply.

5.

According

to SEMI, the semiconductor industry or the supply chains includes integrated

device manufacturers; semiconductor foundries (fabrications); fabless chip or

IC design firms; assembly, testing, and packaging (ATP) service providers.

Sometime it also includes wafer fabrication equipment and metrology tool

vendors; semiconductor wafer and chemical suppliers; electronic design methods

and automation software providers. In the broader microelectronics ecosystem,

it further includes electronics systems companies, researchers, and educators.

6.

According

to definition of SIA, IDMs are vertically integrated across multiple parts of

the value chain, performing design; fabrication; and assembly, packaging and

test activities in house. Some IDMs have hybrid “fablite” models where they

outsource some of their production and assembly.

7.

Semiconductor

production also depends to a substantial extent on neon supplied by Ukraine.

Ukraine supplies more than 90 per cent of US semiconductor-grade neon, critical

for lasers used in chipmaking. Yoon, J. (2022), “The Lex Newsletter: Bright

prospects for neon price dim chip outlook” (Financial Times, 2 March 2022)

8.

The

figures are calculated by semiconductor industry value added by activity and

region, 2019, SIA.

9.

According

to definition of SIA, IDMs are vertically integrated across multiple parts of

the value chain, performing design; fabrication; and assembly, packaging and

test activities in house. Some IDMs have hybrid “fablite” models where they

outsource some of their production and assembly.

10.

IEK, ITRI.

(2022), 2021 Semiconductor Industry Yearbook of Taiwan.

11.

Taiwan

government lifted restrictions of 200 mm wafer fabrication in China in 2006,

and in 2016 approved TSMC’s investment of a 300 mm wafer fabrication in

Nanjing, China.

12.

FACT

SHEET: Biden-Harris Administration Bringing Semiconductor Manufacturing Back to

America | The White House, JANUARY 21, 2022

13.

Semiconductor

Market - Global Industry Analysis, Size, Share, Growth, Trends, Regional

Outlook, and Forecast 2021 - 2030, Precedence Research, 2022. precedenceresearch.com/semiconductor-market

14.

FACT

SHEET: Biden-Harris Administration Bringing Semiconductor Manufacturing Back to

America - The White House.

15.

In the

1980s, the U.S. had more than 200 IDM (as distinguished from Fab-lite and

fabless) semiconductor manufacturers, but many of them were sold, merged

dissolved, or liquidated over the past decades. There were also nearly 180 U.S.

universities and colleges which offered semiconductor programs.

16.

Testimony

of Dr. Tsu-Jae King Liu, Hearing on “Strengthening the U.S. Microelectronics

Workforce,” House Committee on Science, Space, and Technology, Subcommittee on

Research and Technology, February 15, 2022. https://science.

house.gov/hearings/strengthening-the-us-microelectronics-workforce

17.

Taiwan

Ministry of Economic Affairs (MOEA) adopted the “Tai-shang (臺商) Return to Taiwan” Program since 2018 by providing tax

breaks, financial subsidies and assistance in locating lands and recruiting

workforce in Taiwan. As of end of 2021, it was reported that around 1,100

companies were approved under the Program, together attracting $ 1.5 trillion

NT dollars and creating 120,000 jobs.

18.

President

Tsai Ing Wen adopted the New Southbound Policy (NSP) in 2016 and further

released the ‘Invest Taiwan”, or “Taiwan Business Returning Home”, program in

2018, targeting Taiwancompanies in China to remove their operations back home.

Details of the Invest Taiwan program can be found at:

https:://investtaiwan.nat.gov.tw/showPage?lang=eng&search=serviceCenter_07.

Also see Glaser, B. S., Kennedy, S., Mitchell, D., Funaiole, M. P., Center for

Strategic and International Studies (Washington, D.C.). (2018). The new

southbound policy: Deepening Taiwan’s regional integration: a report of the

China Power Project. https://southbound.csis.org/ (last visited April 4, 2022)

19.

Some

of the benchmark projects are Foxconn’s investment in Wisconsin State in 2017

and TSMC’s project in Arizona State.

20.

In

December 2021, TSMC announced a decision to establish a subsidiary in Kumamoto,

Japan in joint venture with Japanese partners. The plan is to build a 12-inch

wafer fabrication with production targeted to begin by the end of 2024.

21.

GlobalWafers,

based in Hsinchu Science and Industrial Park, Taiwan, specializes in 3” to 12”

silicon wafer manufacturing. Its product applications have extended through

power management, automotive, IT and MEMS.

22.

TSMC

has more than 3,000 suppliers from the world. It identifies key suppliers to

provide direct on-site support. These suppliers are not eligible to subsidies

from CHIPs Act, but may be eligible to tax credits from Federal or State

government of Arizona.

23.

FACT

SHEET: U.S.-EU Establish Common Principles to Update the Rules for the 21st

Century Economy at Inaugural Trade and Technology Council Meeting, SEPTEMBER

29, 2021https: //www.whitehouse.gov/briefing-room/statements-releases/2021/09/29/fact-sheet-u-s-eu-establish-common-principles-to-update-the-rules-for-the-21st-century-economy-at-inaugural-trade-and-technology-council-meeting/

24.

FACT

SHEET: President Biden Announces the Americas Partnership for Economic

Prosperity JUNE 08, 2022, https: //

www.whitehouse.gov/briefing-room/statements-releases/2022/06/08/fact-sheet-president-biden-announces-the-americas-partnership-for-economic-prosperity/

25.

Goodman,

Matthew., Reinsch, William. CSIS. (2022). Filling in the Indo-Pacific Economic

Framework. https://www.

csis.org/analysis/filling-indo-pacific-economic-framework?msclkid=c41570d4c62011ec9c4756938a5e21ce

(last visited April 4, 2022)

26.

Taiwan

investments in Southeast Asia highly concentrate in manufacturing sectors,

ranging from labour intensive industries, such as textile and apparel and

footwear, to more technology-intensive industries, mainly Information and

Communication Technology (ICT) and electronics industry.

27.

Hsu,

Kristy T.T. (2022). Taiwan Investment in Southeast Asia: The Choice of Taishang

and Their Response in the Changing Asia. To be published in end of 2022.

28.

Vietnam

has become the fastest growing supplier of ICT and electronics products since

2018, owing to increasing investments from Taiwan into North Vietnam to avoid

the 301 tariffs if they export products directly from China to the U.S. India

has also benefitted from relocation of supply chains of electronics products to

the country. Wistron, a Taiwanese company, was the first foreign manufacturer

to assemble iPhone in India, followed by Foxconn and Pegatron, both Taiwanese

companies. Taiwan’s Pegatron follows Foxconn and Wistron to make iPhones in

India, Taiwan News, July 17, 2020. https:

//www.taiwannews.com.tw/en/news/3968775

29.

Suzuki,

Hiroyuki. (2021). Building Resilient Global Supply Chains in the Geopolitics of

the Indo-Pacific Region. https://

csis-website-prod.s3.amazonaws.com/s3fs-public/publication/210219_Suzuki_Global_Supply.pdf?DJzRt8ACjVJAKaikeMd8mToyxoByQ6B8

(last visited April 12, 2022)

30.

SEMI,

American Semiconductor Academy. (2022). Fuel American Innovation and Growth, A

national Networks for Microelectronics Education and Workforce.